Posts with tag 'Market Report'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2026 | 14 Posts

- 2025 | 24 Posts

- 2024 | 24 Posts

- 2023 | 39 Posts

- 2022 | 75 Posts

- 2021 | 57 Posts

- 2020 | 49 Posts

- 2019 | 9 Posts

21

Finding a New Home for Your Next Stage of Life

|

25

Crazy Prices: What's Really Driving Up the Cost of New Homes

From the March 2021 issue of @Home with Coldwell Banker Tomlinson. Written by Chris Canning, Coldwell Banker Tomlinson Realtor®

As both a licensed REALTOR® and home builder, I often scroll through my Facebook feed and see homes advertised by our area homebuilders and fellow real estate agents. I often see such remarks as: "They want how much for that house? They're crazy!" or "Why can't builders build more affordable homes?" The g...

10

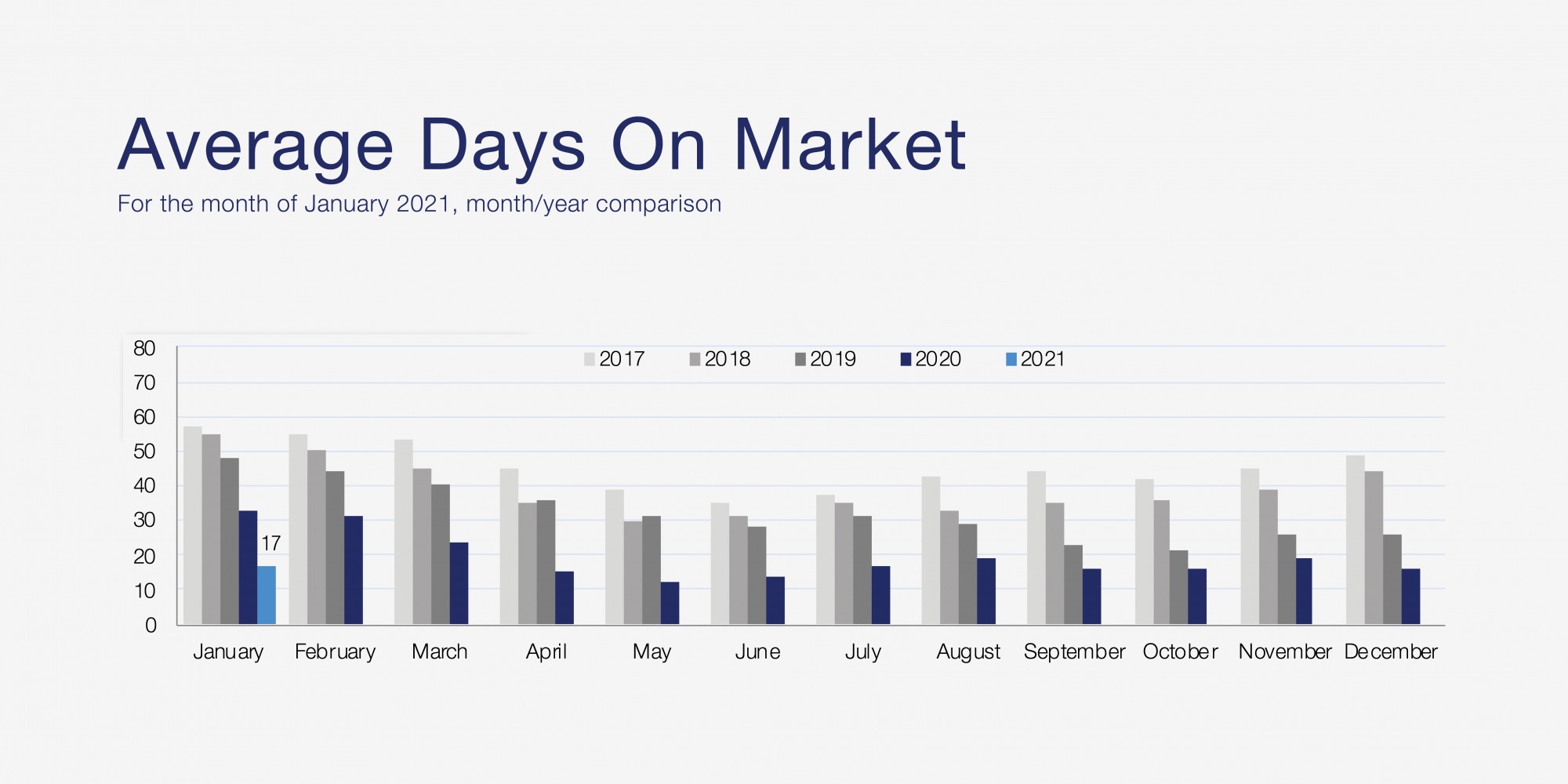

Coeur d'Alene Real Estate Market Report - January 2021

View our comprehensive Coeur d'Alene real estate market report for the month of January!

The information in this report is compiled from a report given by the Spokane Association of REALTORS© and to the best of our knowledge is accurate and correct.

10

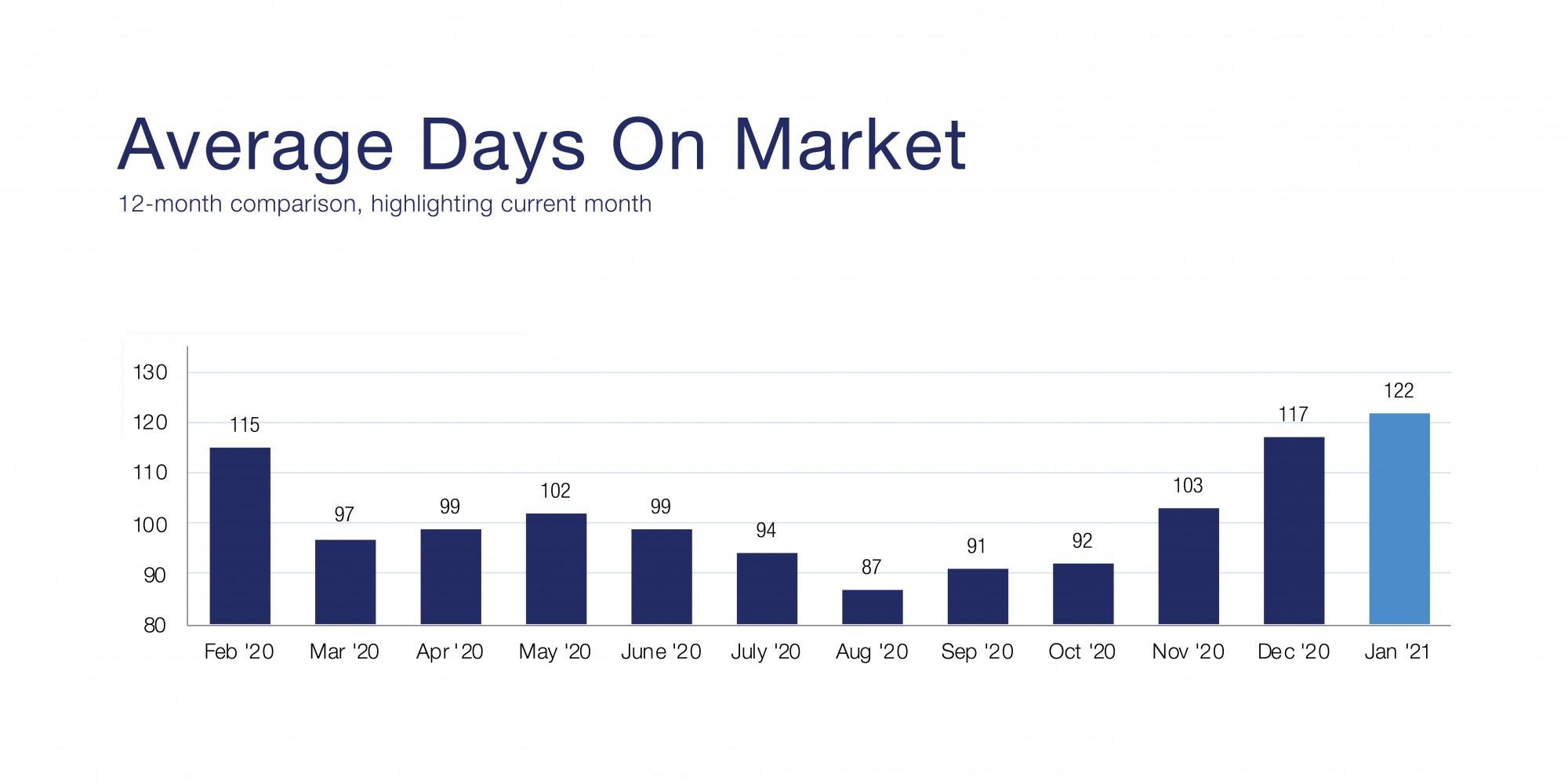

Spokane Real Estate Market Report - January 2021

View our comprehensive Spokane real estate market report for the month of January!

The information in this report is compiled from a report given by the Spokane Association of REALTORS© and to the best of our knowledge is accurate and correct.