Posts from September 2020

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2026 | 14 Posts

- 2025 | 24 Posts

- 2024 | 24 Posts

- 2023 | 39 Posts

- 2022 | 75 Posts

- 2021 | 57 Posts

- 2020 | 49 Posts

- 2019 | 9 Posts

30

Annual Coats 4 Kids Drive More Important Now Than Ever

From the September 2020 issue of @Home with Coldwell Banker Tomlinson. Article written by Cindy Hedin, Coldwell Banker Tomlinson REALTOR®.

With fall just around the corner, we at Coldwell Banker Tomlinson are beginning to gear up for our annual Coats 4 Kids campaign with KXLY 4 News Now. Though, due to the current COVID pandemic and school closures, the Coats 4 Kids campaign will look a little different in 2020, its success is more urgent than ever!

Coats 4 Kids is an area-wide annual fall event and has several local sponsors, including Coldwell Banker Tomlinson. In addition to its corporate contributions, Coldwell Banker Tomlinson Realtors® throughout our region have worked in the past as liasons with local schools...

28

5 Things You Need to do After Buying a Home

After buying a home, you may feel as if you've completed a marathon and are due for a little downtime to settle in and rest. But don't sit too long; there's still plenty to do.

We recommend prioritizing the many must-dos that will ensure your safety and comfort in your new Spokane home. Here are five things to get started on.

21

Lowest Mortgage Rates In History: What It Means for Homeowners & Buyers

In July, the average 30-year fixed-rate mortgage fell below 3% for the first time in history.1 And while many have rushed to take advantage of this unprecedented opportunity, others question the hype. Are today's rates truly a bargain?

While average mortgage rates have drifted between 4% and 5% in recent years, they haven't always been so low. Freddie Mac began tracking 30-year mortgage rates in 1971. At that time, the national average was 7.31%.2 As the rate of inflation started to rise in the mid-1970s, mortgage rates surged. It's hard to imagine now, but the average...

14

Scenic Spots Around Spokane to See Fall Colors

It's hard to believe summer is almost over, but there will be a nip in the air before you know it! As summer turns into autumn, we all look forward to the stunning fall foliage that Washington is known for. This is one of the reasons why we love showing homes in the autumn months.

When we speak with potential buyers who are new to the area, we always recommend that they take a short break from exploring Spokane homes for sale to visit some of the area's most scenic spots. Here are a few of our favorite recommendations.

11

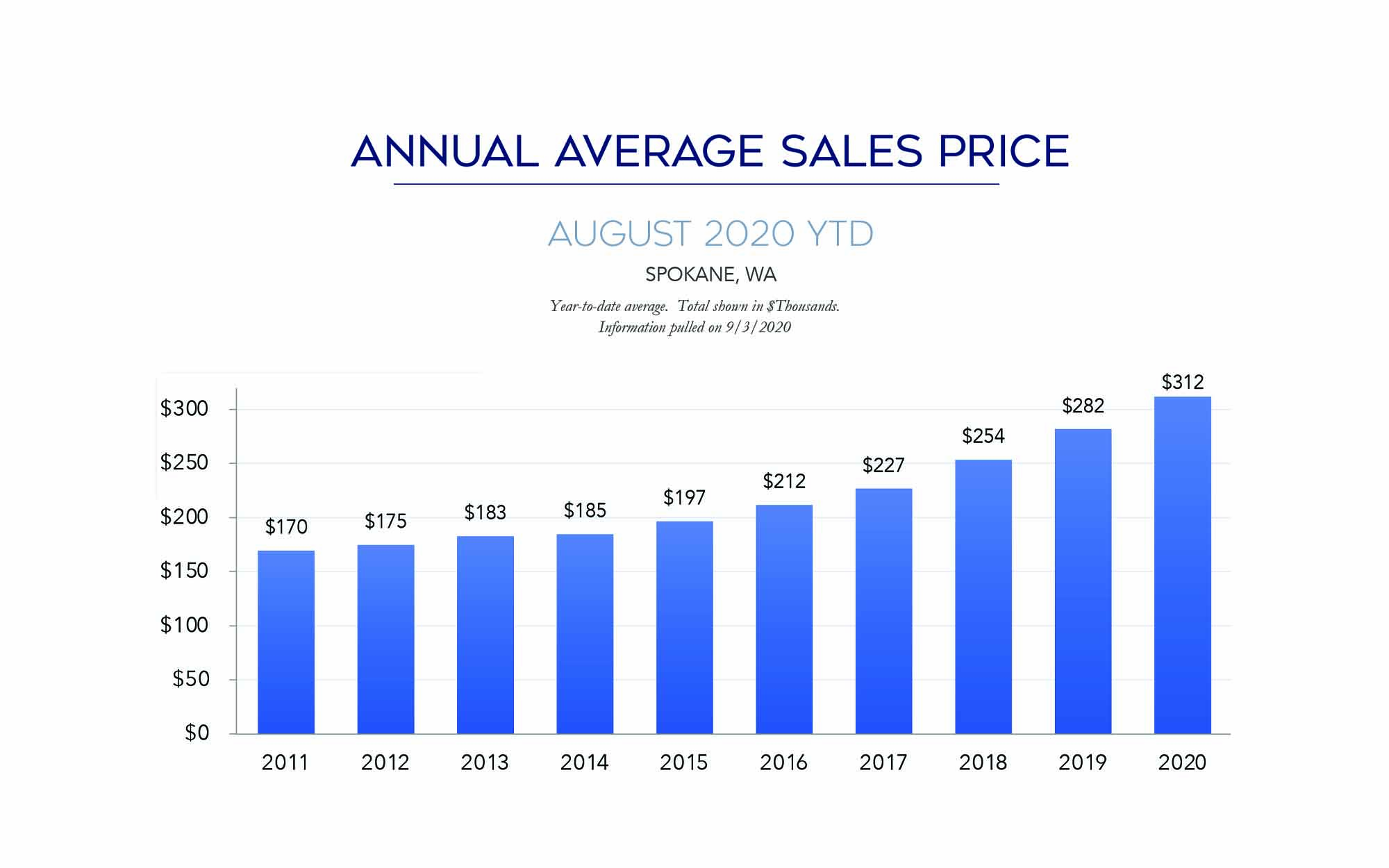

Spokane Real Estate Market Report - August 2020

View our comprehensive Spokane real estate market report for the month of August!

The information in this report is compiled from a report given by the Spokane Association of REALTORS© and to the best of our knowledge is accurate and correct.